Ownership vs Loanership

Posted by Orrin Woodward on June 17, 2014

The glory of Western Civilization was its protection of life, liberty, and property. Through an admixture of Biblical principles, Natural Law, and the English Common Law, America was gifted a solid foundation for people to enjoy a life of liberty with protection of private property.

Today, however, this historic legacy is under attack. Perhaps the most significant attack is the one least understood by the people – the State supported Fractional Reserve Banking (FRB) system imposed upon society. What is this FRB system? In short, it is the State sponsored process whereby banks use customer deposits as a fractional reserve base for loans to third parties. Loans of deposits is not fraudulent, but when the State permits the bank to turn a $1,000 deposit into $10,000 worth of loans, then we have an ethical problem.

Fractional Reserve Banking Creates Money

According to Professor Thorsten Polleit of the Frankfurt School of Finance and Management, FRB, “means that a bank lends out money that clients have deposited with it. Fractional-reserve banking thus leads to a situation in which two individuals are made owners of the same thing. Fractional-reserve banking thus creates a legal impossibility: through bank lending, the borrower and the depositor become owners of the same money. Fractional-reserve banking leads to contractual obligations that cannot be fulfilled from the outset.”

Anyone ever heard of a bank run? This occurs when customers are concerned that the bank does not have enough money to redeem all the deposits of its customers. Of course, in the FRB system, the bank doesn’t have all the depositor’s money since it has loaned it out many times over. Only the minimum fractional reserve mandated by the State is retained to service potential depositor withdrawals.

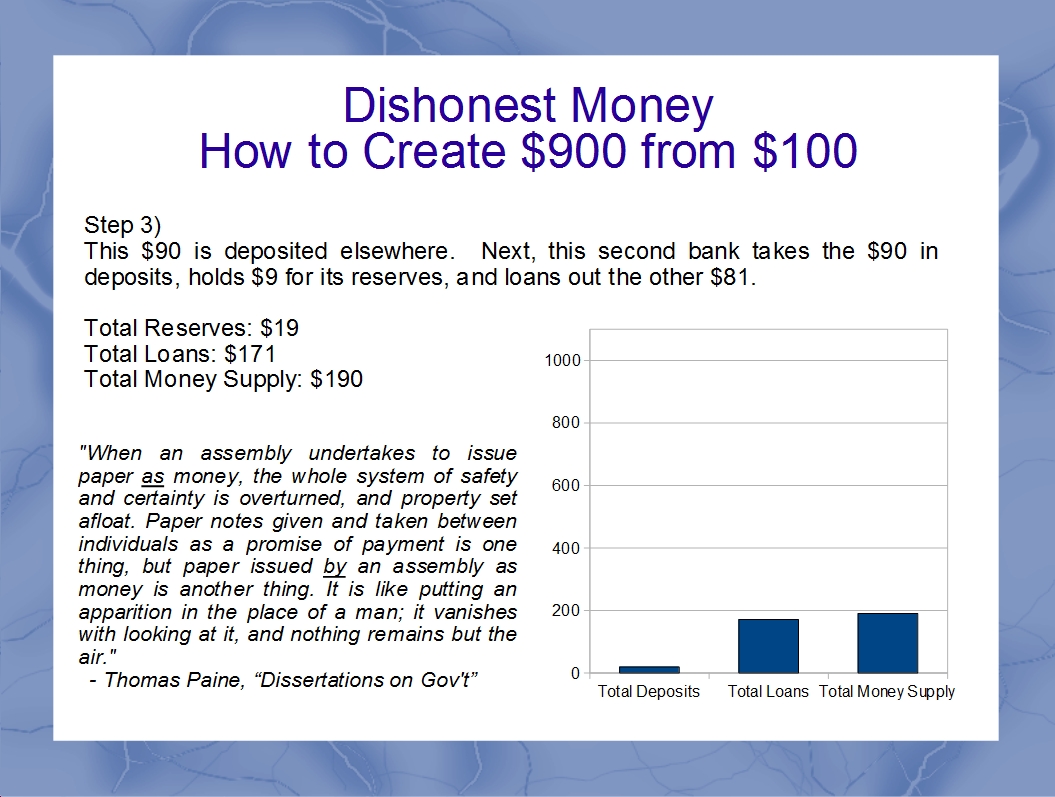

In truth, every FRB bank is inherently bankrupt by the very nature of the State allowing only fractional reserves. Proverbs 11:1 states, “The LORD detests dishonest scales, but accurate weights find favor with him.” Alas, FRB is dishonest because it pyramids fiat money (dishonest layers of fake money) on top of the real money deposits.

By studying the FRB system, one quickly realizes that it permits the banks to expand the money supply (leading to inflation and boom/bust cycles) by loaning the same deposited money to numerous other individuals and businesses. Somehow the banks profess to have the money on deposit for immediate withdrawal while, at the same time, providing the funds several times over to other parties. Banks, through the joys of the FRB system, can charge interest on loans that exist only on a computer screen or on a piece of paper not backed by real deposited funds.

How, for example, can $1,000 of real deposits be converted into $10,000 of loans? This is nothing less than creating money out of thin air. Worse, this fiat money is dangled in front of instant-gratification consumers, who do not possess the moral strength to delay their gratification until they have produced enough income to pay cash for the desired item. Instead, they eagerly enslave themselves into the FRB system for the latest of Mammon’s creations.

Indeed, the number one method the FRB system captures people into its net is through the consumers desire to “own” a house. Whereas in 1900 there were only 5% of the households in America holding a mortgage, today that number has ballooned to over 37%. The rapid increase in the number of mortgages is responsible for FRB mortgage debt money becoming over 70% of the total USA money supply at its peak! No wonder the State and FRB system are constantly reducing the qualifications for home ownership because its the easiest way to ensnare people into usurious debt.

The State sponsored FRB banks needs the populace to remain in debt in order to fund the debt-based monetary system. This is not just my personal opinion on the issue, but is well-known, though rarely discussed, fact by those in power. For instance, Robert H. Hemphill, credit manager of the Federal Reserve in Atlanta, stated in 1939:

If all the bank loans were paid, no one would have a bank deposit and there would not be a dollar of coin or currency in circulation. This is a staggering thought. Someone has to borrow every dollar we have in circulation, cash or credit. If the banks create ample synthetic money we are prosperous; if not, we starve. When one gets a complete grasp of the picture the tragic absurdity of our hopeless position is almost incredible, but there it is. It (the banking problem) is the most important subject intelligent persons can investigate and reflect upon. It is so important that our present civilization may collapse unless it becomes widely understood and the defects remedied very soon.

Simply put, the entire system relies on people willingly enslaving themselves into the FRB system. Ok, I have ranted long enough. Is anyone interested in the solution?

Consumers, en masse, must reject the FRB model of increasing debt to “own” products. Instead, they must pay for goods today from production they earned yesterday. Simply put, its time to build Ownership rather than Loanership. Laurie and I personally made the last payment on house in Grand Blanc in early 2003 and have been out of the FRB system ever since. It is LIFE Leadership’s goal, through sharing the principles in our Financial Fitness Pack, to help millions of others get free from the FRB system.

Jesus said, “No man can serve two masters: for either he will hate the one, and love the other; or else he will hold to the one, and despise the other. Ye cannot serve God and mammon.” No, I am not saying to sell your house and live like a hermit. But I am saying to eliminate debt in your household like a patient seeks to eliminate cancer from his/her body. As one wipes out debt, start paying down the mortgage principle down by restraining one’s urge to spend until it is paid off.

LIVE DEBT FREE! Then, and only then, can a person experience both spiritual and economic freedom to follow God’s plan rather than Mammon’s commands.

Sincerely,

25 Responses to “Ownership vs Loanership”

Sorry, the comment form is closed at this time.

Elizabeth Sieracki said

In growing communities I would say Finances is one of the biggest issues people deal with on so many levels. I am so thankful we have the FFP and other materials to help people find solutions. Thank you.

Larry Allswede said

Wow!! I can’t tell you how tempting it is to play ownership with loanership! Again, Wow. Thank you for the perspective. Operation financial-cancer removal starts effective immediately!

Steve Leurquin said

I was going to reply with a “Wow!” but then I saw Larry’s response and thought I would be original, Holy Wow! This will be hard for many to read, including myself, but the truth rings sweet to the ears! Thanks for sharing what many don’t want the public to know.

Steve

Ed Fancon said

Orrin, there isn’t much you write I don’t like. Come to think of it, I cannot pinpoint one example. However, I LOVE this explanation you give regarding the FRB. Thanks so much for all you’ve done for those around you. See you in Columbus!

Clint Fix said

Well said Orrin! I have never understood why people buy into the FRB system so easily. Maybe they think that’s how it has always been? It always seemed like a massively dishonest system. I’m proud to be associated with a community that’s educating people about issues like this.

Steve Meixner said

Orrin, So glad to be a Part of this Company! I have learned so much and though I am not there yet, I will be one of those Debt Free People, never to be a Slave of the FRB System again!! Thank You,

Steve

Bart Springer said

Orrin, you’re saving this star fish!

David Nelson said

The US Government is making sure people stay in debt by promoting casinos all around the country. Currently New York State is promoting building casinos along the Thruway running from NYC to Buffalo. Imagine having a casino, built with FRB funds, in every town to suck up every last dollar from the people who can’t afford to lose what little money they earn. It seems like a big push to destroy life or usher in the ultimate deceiver who will have a mob willing to capitulate similar to the countries who voted in Hitler.

curtis shaw said

Larry nailed it. Fantastic article.

Danielle Bercier said

Unfortunately the average Joe is willing to look away and needs to be better informed about his own finances, because the information we receive from advertisement is so misleading, and you wouldn’t know because you may not have the right information! I love what we stand for in Life Leadership and appreciate your teachings of a better way of Life, no pun intended. I didn’t realize the reality of the situation. We’ve been able to make a change in our lives thanks to the Life organization and we hope to be able to help make a difference in other people’s lives.

Scott Staley said

Great article. In our instant gratification society – the scales are really tipped towards Loanership (I love Claude’s concept that all items should be pink if they’re purchased on credit – because then we’d all know what the Jones’s really have!). Having just gone through a local election here (Ontario Canada) where the winning party advocates spending OPM, how can we help swing the scales back the other way(quickly)? I feel like the fox is in the chicken coup – and my freedom(s) are the chicken!

Randy Robson said

Great article!

Olivier Jean-Baptiste said

Hi Orrin

Thanks for your post.

Personally, below is the sentence from your post that SHOULD be reflected upon deeply by all.

“The State sponsored FRB banks needs the populace to remain in debt in order to fund the debt-based monetary system.”

That “debt-based monetary system” is truly the whole “camel herd in the tent”.

Referring to the foreign vested interests entangle to such debt-based monetary

system, Andrew Jackson seems to equate it to a matter of national sovereignty when he said the following in his veto message regarding the re-chartering of the Bank of the United Sates:

“All its operations within would be in aid of the hostile fleets and armies without. Controlling our currency, receiving our public moneys, and holding thousands of our citizens in dependence, it would be more formidable and dangerous than the naval and military power of the enemy.”

How unfortunately accurate his predication have come to be manifest in today’s landscape.

Fortunately Life Leadership is here to ignite hope, educate and revers the current of decline.

thanks,

Olivier

Antoniorosselli said

It is interesting to see that in the first half of the previous century … A culture of debt already existed …

It is very fascinating to learn how the monetary mechanism works … At least parts of it …

I agree with staying away from debt if possible … Especially if there is no good reason to borrow money …

*Trivia : ” Standard oil is an example of a company that expanded its concerns by borrowing from banks … Same with wall mart too … Just to make a couple of examples …

Maybe i should start to lend the same dollar to 10 different people … And collect interests …

Thank you for the post …

JeanetteP said

Hi Orrin,

I am also curious what you may know about a gentlemen who was at the signing of the constitution whom supposedly interrupted the “arguing” that was going on right before it was signed, to declare America as the will of God (I think that’s what he said) and thus they all signed. Anyway, I believe he was dubbed “the Proffessor”. Do you have any more info on the mysterious guy?

Last but not least, thank you for continuing to fight for the Truth and all that you and Laurie do!

God bless and keep you!

Jeanette Pike

Orrin Woodward said

Jeanette, My email is to the right on this blog under email me. Please feel free to send along your vision. thanks, Orrin

Shaun Bushey said

You’ve definitely delved into one of my passions and nailed it on the head! There’s so much to be said but so little needs to be between the FFP, the FF series and your upcoming best selling trilogy. I personally think George Bailey’s simple explanation in “It’s a Wonderful Life” of FRB is proof that it’s by design and it’s been around for a long time. Thanks Orrin for being a beacon in the fog.

Ernie Reeves said

Well articulated, sir!!

Kerstin Schaefer said

Orrin

Thank you, thank you, thank you for putting hard to understand issues into simple language so that even this German girl can get it. We appreciate your drive for education so much. God bless you and all the other leaders.

Steve Sager said

Wow! As I read this it scares me to know, that this information is NOT being taught at the high school/college level… Where a lot of financial decisions are made with loans. Yikes! So thankful for the LifeLeadership information.

Peggi Kern said

Thank you, Orrin for your blog and continuing to educate!

Blaine Terrill said

Such timely truth! I hope all who read this will share it with every leader worthy of following they know personally!

Terry Rutland said

If what u say is true, we the people have been trick,fool & deceived. by the government and the banking community, having us believe that loanership is best for all parties involved. Thanks for the insight

Chris Olson said

truth

Scott Allen said

Investor/author/entrepreneur James Altucher has a couple of great articles on this, making the case that even if you have the money to buy it outright, owning a home may not be the best answer:

Why I Am Never Going to Own a Home Again

It’s Financial Suicide to Own a House