Once the elites understood how much wealth could be pilfered from society by capturing the money supply, it was not a question of free money or controlled money. Indeed, the only real question was: who would control the money system and whether it would be led by State Power creating a national fraud or by the Money Power creating an international fraud.

In reality, it wasn’t much of a contest since the Money Elites knew the State’s Achilles heel – it’s all-consuming desire for more power. To increase the State’s power over society, at least in a money economy, the State must direct more of society’s resources, which is just another way of saying the State needs more money. This is a challenge for a States in every age but was especially problematical in the classical age when the money system of society consisted mainly of gold/silver coins. As a result, there were only two ways for the classical States to access more funds, namely, increase taxes or borrow money. Remember, this is before State had the ability to print paper money because this fraud had not been discovered yet. Society, in any event, would not have recognized it as money anyway since precious metal coins were used as money. The State elites (monarchs, emperors, and tyrants) found increased taxes harmed their popularity with the people; hence, they saw the Money Power as the lesser of two evils. The monarchs, choosing short-term good for longterm harm, simply borrowed money from the financial elites rather than upset their subjects by increasing taxes.

Master of the Puppets

The State, strangely enough, despite owning the “monopoly of force”, feared a current tax rebellion more than a future debt slavery. Ironically, it will probably end up with both. The State elites sold the nation’s financial future (freedom decreases as debt increases) for increased power in the present. Meanwhile, the savvy financial elites did not rely on just one State for profits. Indeed, they offered loans to every rival States to generate competition amongst the States, which increased the total debt and expanded their financial web. The Money Power, after all, understood as State debts increased, they could demand further privileges to ensure mastery over the State. The Money Power (international elites) now topped the power pyramid followed by the obedient State Powers (national elites) which then directed Societal Power (the masses). Over time, the State, regrettably, became just as oppressed by the Money Power as the people were by the State and Money Power combination.

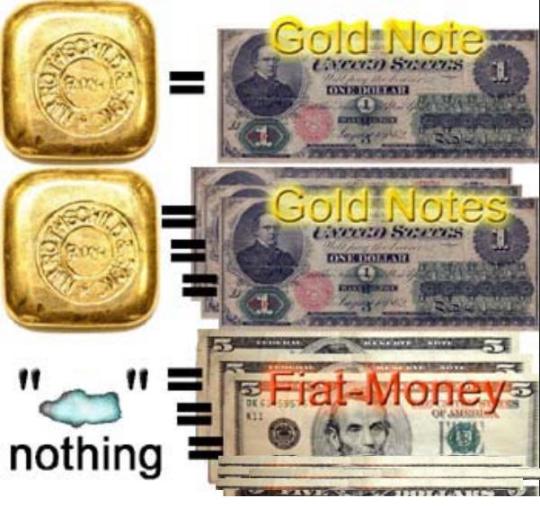

Unfortunately, the bad news gets even worse. For the “loans” used to enslave the States were not based upon real gold and silver stored in bank vaults; instead, the international financiers used what is known as fractional-reserve-banking (FRB) to initiate numerous loans with only a fraction of gold/silver promised in reserves. In a word, the States enslaved themselves by loving money more than the people. Through the use of bank ledgers credits and an early form of bank note credits, the States accepted money created out of thin air, but forced the people to pay back the loans with precious metals! One may ask how the same precious metals can be loaned to numerous parties (States) at the same time? In the real world, this is physically impossible, but in the imaginary world of high finances, it is metaphysically possible (bank ledger notations) despite being morally impermissible.

It’s been said there is nothing new under the sun, only the history a person doesn’t know. The modern States seem to validate this statement as they appear to have learned nothing from their ancient predecessors – both borrowed themselves into bankruptcy. The Money Power has mastered the State and society with FRB loans created out of thin air. While this information may seem shocking, it is true nonetheless. Yes, the truth will set a person free, but usually only after it ticks him off.

The author has termed the private Money Power’s control over the banking system and money supply the Financial Matrix – a system of control where the Money Power creates money out of thin air to loan to society’s members for profit and power. The origins of the Financial Matrix can be traced back to ancient Babylonian banking practices. In the early twentieth century, however, with the creation of central banks as lenders of last resort, the Financial Matrix now reigns supreme over the earthly world. This debt system not only enslaves individuals and captures corporations into debt, but it also neuters the nation’s of the world. The Bible admonition in Proverbs 22:7, “The borrower is slave to the lender,” could not be more relevant than it is today and each person must face up to what role he is playing with respect to the Financial Matrix.

For instance, when a person borrows money to buy things he does not need, he is feeding the matrix and losing his liberties. The people must learn to deny themselves short-term pleasures in order to avoid the longterm pain. One final bitter fruit of the Financial Matrix system is the stress and pain experienced when a person attempts to pay off debt with compound interest working against him. The profits and control, in effect, go to the Money Power while the pain and stress go to the debtors. Financial ignorance is not bliss but rather pain personified. When the State debt increases the governments must squeeze society for more tax dollars even though the people are already struggling with their own debt. The shortfall, is then made up by the State borrowing even more money that it cannot afford. This is a form of insanity. Unquestionably, the kick the can down the road strategy cannot last but today’s politicians hope to be out of office by the time the can is no longer kickable. 🙂 Politics is now like a game of musical chairs where the current political leader hopes he is out of office before the music stops.

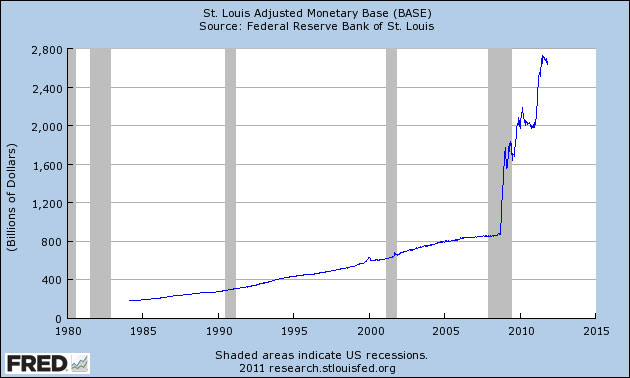

Meanwhile, the St. Louis Federal Reserve announced the total US debt (the combination of government, business, mortgage, and consumer debt) has risen from $2.2 trillion total in 1971 (the year Nixon took the dollar and thus the world off the gold standard) to $59.4 trillion in the first quarter of 2014. This is not a typo. The debt in America, which took nearly 200 years to reach $2.2 trillion and included the debts from the Civil War, WWI, and WWII, is now (43 years later) 27 times higher! Even at just 5% interest, this amounts to over $3 trillion in interest to service the debt. That’s 3,000,000,000,000 dollars every year, which is more than our total debt was a mere 43 years before. What is going on?

When Nixon took America off the gold, the dollar still remained the world’s money system, but it freed the Money Power to create as much money as it wanted without and need for gold in reserve. This turbo-charged the ability of the Financial Matrix to loan money and the consumers naively accepted the bait. I believe it’s time for the citizens of the world to reject the debt seduction. True, you can, like the proverbial ostrich, put your head in the sand and ignore this entire article, but I promise you even though you may hide your head from the financial tiger, it will still be painful when you are devoured. 🙂

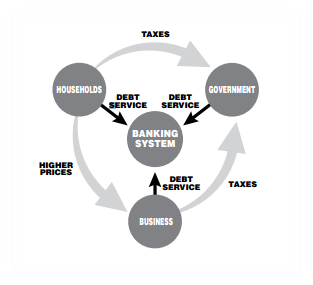

The chart below reveals how the Financial Matrix is siphoning off trillions of dollars of productive capacity in each nation. The debt for American governments, corporations, and individuals is now around $20 trillion each and the interest payments are causing significant price, tax, and debt payment increases. The average American family is at the breaking point and what is need is some financial wisdom to alleviate their personal debt and stress. There is a personal pathway out of the Financial Matrix and I promise to do my part in sharing the steps to freedom.

Without intending to sound overly dramatic, I truly believe this is liberty’s last stand. The Founders of LIFE Leadership intend to stand in the gap and educate the masses of the world on a plan to escape the Financial Matrix. Will you help us set the captives free?

Sincerely,