Western Civilization’s Debt Trap

Posted by Orrin Woodward on July 11, 2014

Western Civilization is in the midst of a life and death struggle with its monetary system. The financial elites have bound society with the most oppressive monetary system ever created, where over 90% of the money supply exists through debt. This is a recipe for disaster as people, companies, and governments at all levels are chronically insolvent.

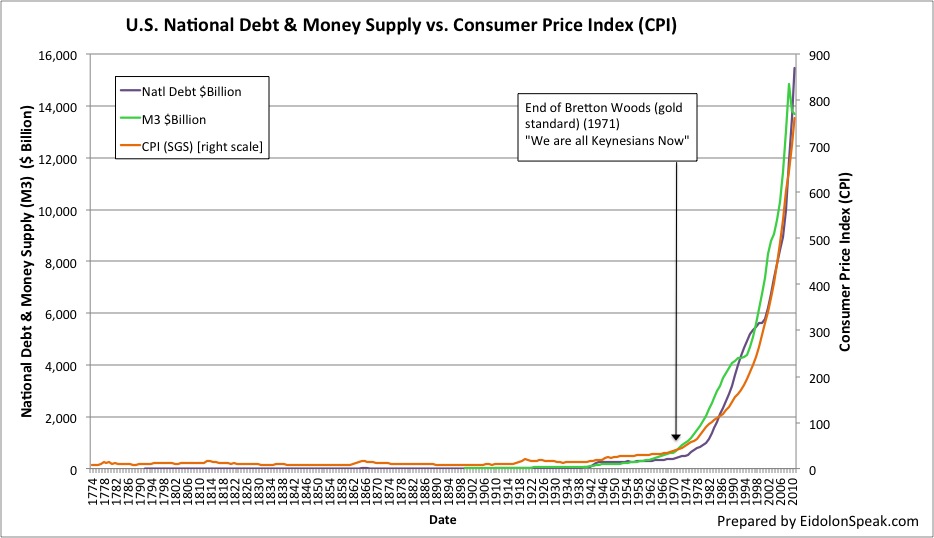

Money Supply Explodes Without Gold Standard

While reform of the total monetary system is essential, individuals should not wait for global reform to begin household reform. Indeed, the best thing for each person to do is launch a financial revolution where he lives below his means and wipes out ALL of his debt. This includes student loans, car loans, and even mortgages. In the process of wiping out out personal debt, one also reduces the money supply created by that debt.

It’s really a simple, but not easy choice. Does society want products and services so badly that it will sell itself into debt-slavery in order to obtain them? Or, on the other hand, can society learn to apply the three keys to wealth to its finances by taking a longer term perspective, delaying its gratifications for trinkets, and start leveraging the effects of compounding to its benefit.

Sadly, our society does the opposite today by viewing everything in the short-term, desiring instant gratification, and having compound interest work against them. LIFE Leadership has committed to play its part in helping people, companies, and governments get out of debt by applying the proper principles of financial management. Indeed, it all starts with the individual. When a person decides to end his debt-enslavement, he becomes the model for others to follow. The Financial Fitness Pack has already helped thousands of people terminate their debt and it can help others do the same. Are you sick and tired of running out of money before running out of month?

The financial debt matrix is real and continues to grow. Ignorance only imperils one’s financial health. British monetary reformer Michael Rowbotham explained the effects of the debilitating debt system upon Western Civilization when he wrote:

The reason for all this monetary scarcity and insolvency is that the financial system used by all national economies worldwide is actually founded upon debt. To be direct and precise, modern money is created in parallel with debt. The reason for the failure of economists to question patently invalid monetary data becomes clear – there is a total acceptance by them of the most extraordinary method for supplying money to the modern economy.

The creation and supply of money is now left almost entirely to banks and other lending institutions. Most people imagine that if they borrow from a bank, they are borrowing other people’s money. In fact, when banks and building societies make any loan, they create new money. Money loaned by a bank is not a loan of pre-existent money; money loaned by a bank is additional money created. The stream of money generated by people, businesses and governments constantly borrowing from banks and other lending institutions is relied upon to supply the economy as a whole. Thus the supply of money depends upon people going into debt, and the level of debt within an economy is no more than a measure of the amount of money that has been created…

If a monetary system is invalid or flawed, then the entire economy is based on the mathematics of error, and must be riddled with the effects. If the financial system upon which our economies are built is defective, and yet monetary considerations dominate our economic decisions, should we be surprised if the results are less than satisfactory?

The major role played by bank credit, which forms over 95% of the money stock in most developed nations, suggests that it cannot but be implicated in these trends. This is further suggested by the way that banking has literally become the focal point of modern economic management, through manipulating interest rates. The stargazers of Whitehall and the Federal Reserve hold their councils, trying to tread the non-existent tightrope between growth and recession by debating quarter percentage-points of interest rates. Alan Greenspan, the Chairman of the Federal Reserve, engagingly describes his task in controlling the American economy through adjusting interest rates as a matter of ‘taking the champagne away once the party has started’. Businessmen around the world hold their breath, measuring his every word, wondering what he will decide. There could be no greater indictment of contemporary financial economics than this; that a fluctuating financial digit on a single computer system in a single street in a single country should have the ability to dominate the economies of an entire planet…

The past thirty years are almost unique by comparison with the previous three centuries in the lack of attention that has been directed at debt and the financial system. Throughout the eighteenth century, there were repeated calls for reform. During the nineteenth century, excessive banking was held by many to be directly responsible for the waves of appalling poverty that swept Europe and America during a period of increasing industrialisation and agricultural development. In this century, during the depression of the 1930s, the financial system effectively seized up and brought virtual collapse to the economies of the world in an age which was, perhaps for the first time, obviously wealthy, and in which technology offered people real freedom as well as material prosperity. One observer judged that over 2,000 schemes for monetary reform were put forward at that time – all with a common theme in their outright rejection of the debt-based financial system as it then operated. The same system continues to this day, modified in small details, but unchanged in principle; and the recent financial crisis in Asia shows the potential for collapse still exists.

However the issue of economic volatility through booms, slumps, crises, and collapses has never been the sole point of criticism. It is the long-term trends that a debt-based financial system fosters which are most destructive. The most obvious of these is declining personal solvency. Mortgages support over 60% (£420 billion) of the money stock in the UK and over 70% ($4.2 trillion) in the US. Housing-debt statistics for the UK and the US show that there has been a dramatic decline in true home ownership as mortgages become higher and ever more widespread. There can be little question that relying upon housing debt to supply money to an economy lacks economic and political justification. However, taken in conjunction with the marked rise in commercial debt, mortgages have a knock-on effect. In an economy where the price of goods is elevated by commercial debt and consumer incomes are deeply eroded by mortgage debt, there is a persistent and subtle advantage given to low-quality, mass-produced goods, and growth is fostered in this direction. The persistent decline in product durability and the growth-culture of a rapacious consumer society can be directly traced to the debt-based financial system…

The more one explores the broad impact of debt, the more apparent it becomes that bank-credit constitutes a dysfunctional form of money. An economy based almost entirely upon bank-credit and debt experiences an intense drive for growth, regardless of need or demand. Bank credit engenders financial dependence, injects instability and fosters growth-distortions, both within an economy and throughout the international arena.

Reform of the debt-based financial system is clearly not a minor issue. It is not a matter of fiddling around with taxes, incomes and allowances to make things apparently more equal, more efficient, or perhaps more straightforward. Changing the debt-based financial system involves gradually altering the very foundations upon which national and international economics is based. Monetary reform is concerned with attempting to determine a new principle for the supply of money to an economy – the purpose being to create a supportive financial environment in which more constructive economic trends are allowed to emerge, and in which more benign systems of overall economic management become possible.

Sincerely,

19 Responses to “Western Civilization’s Debt Trap”

Sorry, the comment form is closed at this time.

Steve Otte said

Check out those model, Orrin. Contributionism

george guzzardo said

Orrin, Your efforts in this most important issue will not go unnoticed when leaders in communities like ours sound the battle cry of debt reduction. Many civilizations have been carried off into bondage – slavery. Why would any adult wish to sentence our future generations because they lack the character to solve this issue? The most precious resource of freedom is being taken right from our very eyes without a whimper. As for me and my family, we pick freedom!

Dave Hall said

Orrin, thanks for being one more voice of reason in an age of economic insanity.

Eli Bowman said

What grassroots initiatives exist to demand this change? Are there local programs across the country that Life Leadership supports or sponsors? I’ve been enjoying this blog for several months now but want to take action where Orrin and his team may be involved. What currently exists on a ground level that is supported or organized by Life Leadership?

Orrin Woodward said

Eli, a return to the gold-standard (you can see from the graph in the blog post what happened to the money supply when the last link to gold was removed by Nixon) is the only Six Duties of Society fix to the Five Laws of Decline debt-based monetary system. So Ron Paul and the Austrian Economist seem to have the clearest, most workable fix to bringing the words And Justice For All back to society rather than plunder for the few at the expense of the many. 🙂 You can read further on this in my new book And Justice For All or the previously released LeaderShift. thanks, Orrin

Robby Palmer said

This is why my job is so degrading to me now. I have learned what poison this lifestyle is, debt… To finance what I can’t afford. And all day I sign people up for a service to fix their past lessons of what they can’t afford, on their credit report, so they can go Into more debt. I feel like I’m contributing to the problem.

Oh the pain that could be saved from the slaves of debt. Imagine if this was taught in the public school systems.

Humans by majority tend to be followers, and principles seem to be taught and allowed by the mindset of “everyone else is doing it, and they seem ok, so why not me?”

It’s gotta be stopped. George is right! LIFE leadership can make the change!

Tim Marks said

Orrin

Great post! Most people are totally blind to how serious the debt issue ( crisis) really is. Most believe that if things get too bad “well, we can file bankruptcy and take care of it” at some point it won’t be so easy for citizens personally because our government will be in line ahead of its people.

I’m so thankful for you and the other Life Leadership founders for creating the FF pack to help people understand and fix the financial issues they have.

Thanks!!

Tim

David Nelson said

Orrin, It seems to me the FLD and fractional banking puts a better explanation on why the US Gov. bailed out companies. It wasn’t to save them. It was to stop this fake debt from being exposed. Everyone from a large company to a home buyer uses this fake money debt to finance a project and they could unknowingly be at extreme risk to be wiped out, if one domino falls, as in your example of being able to knock over a larger domino, maybe wipe out someone else who also has used this fake debt. Allowing GM or Bank of America to fail would have eliminated the payments required to keep the fake debt hidden and would have knocked over some major dominoes maybe knocking over larger and larger ones till it hit the federal reserve and BINGO the USA fails. Someone in the Federal Reserve sees what you see enough to know. Someone with major financial power knows what you know and is scared.

You are doing some mighty awesome knowledge revelations and making it easy to understand and interesting.

Where I spent my first 35 years in upstate NY, NYS is trying to convert farm land into casino resorts along the NYS Thruway. Obviously, they don’t get enough tax revenue from income tax, the lottery, and all other taxes, so now in order to keep the dominoes from falling they are going to take more of peoples money by putting in state controlled casinos. It’s crazy.

Sincerely,

Dave Nelson

Orrin Woodward said

David, yes that is correct. The whole debt system would have been wiped out as the dominoes compounded and all of the Big Banks would have collapsed on top of the unethical FRB system followed by many Big Corps with massive short-term debt that must be rolled over daily to weekly. Instead, of course, they shifted the damage onto the SDS producers within society and allowed the FLD exploiters to maintain the plunder. This, however, cannot continue because the debt load increase has maxed the Federal government to the point that they will not be able to bail out the FLD plunderers next time without hyper-inflation. We have a responsibility to fix this for our children and grandchildren’s sake. NOT ON OUR WATCH! 🙂

Danny Kellenberger said

Thanks Orrin for this great information. I sure wish someone had taught me this earlier in my life and helped me understand fractional reserve banking and how debt is created. I look forward to the day I can say “debt” is a four letter word in our house and we have no more of it. Thanks to you and Life Leadership I have quality, credible information to help me on my journey.

Captain Bill Howard said

“Mortgages support over 60% (£420 billion) of the money stock in the UK and over 70% ($4.2 trillion) in the US. Housing-debt statistics for the UK and the US show that there has been a dramatic decline in true home ownership as mortgages become higher and ever more widespread.”

Sounds live serfdom to me! The mortgages are primarily owned by Fanny Mae and Freddie Mac, which is owned by the… Federal Government. This fiat exchange for the American dream gives the federal government control over most of the real estate in the United States. The American public has traded control of their private property to a financially irresponsible bureaucracy who has leveraged their credit (and homes) to go even deeper into debt, (17 Trillion and rising). Orrin you hit the nail on the head, pull the rug out from under these spendthrifts and get out of debt! It only empowers this fractional reserve borrowing scam. Debt is a failure to pay a promise from yesterday.

Jim Wilson said

Oren,

Thank you for your blog. As a very young man in my early 20s in the 60s, I recognize that manufacturing was being driven by consumer debt. I realized then that it was inflating the cost of goods. At that time, I did not equate it with expanding the money supply. Thank you for clarifying that.

Jim Wilson

Joel Avila said

Hi Orrin,

I’m a ‘formally schooled’ dude.. I have a degree in Engineering and an MBA.. I want to scream and shout, and return these high-priced credentials to my alma maters and demand a full refund because they didn’t teach me jack! Thankfully a buddy at the gym introduced me to Life Leadership; so I have begun my journey to being truly educated.

Thank you for what you and the other founders do!!

God Bless.

Orrin Woodward said

Joel, welcome to LIFE. I learned some great stuff in engineering school on systems and logic, but didn’t learn about myself. Until a person knows himself, it is very difficult for him to help others. LIFE Leadership has a mission to change the world one life at a time and it begins when each of us seeks education, not just training. YOU are on your way Joel! 🙂 God Bless, Orrin

Shaun Bushey said

I love the chart, great visual Orrin!

Steve Meixner said

Orrin, Thanks again for the great Information. I will pass it on. This is the best Education a Person can get,

Steve

Miriam said

We are so blessed to get this information at a young age! Thanks for all you do to study this information and package it in a way we can understand in our 20’s!

Scott Allen said

I just came across a speech from earlier this year by William Dudley, president of the Federal Reserve Bank of New York, in which he explains exactly why student loans are a terrible investment for taxpayers, as well as for students:

http://www.bloomberg.com/news/articles/2015-03-04/this-fed-official-just-perfectly-described-why-student-loans-are-a-terrible-investment

Kurt said

Orrin, thanks for explaining our financial system so that the common person can understand. Thanks to the Green Box program, I not only understand principes to my own finances, but now I’m around others that are doing the same. When I am with our community it keeps me on track to my own financial goals. Thanks Orrin!