It’s important to remember that money was not created by the state. Rather, as Mises points out, entrepreneurs created money by trial and error through realizing that gold and silver could be exchanged for current production at any time. Money simply was a measurement of exchange value ratios. Indeed, the rediscovery of gold and silver money led to an explosion of middle-class wealth as people were rewarded for producing more. The gold standard ensured justice for the masses against elites attempts to manipulate the exchange values of monetary system. Because gold is a fixed-quantity and difficult to mine, inflation was low and predictable, whereas the increased division-of-labor caused by the capitalistic system to create more wealth for more people than at any time in recorded history. The gold standard, in short, ensured justice for all by checking the elites desire to create a Financial Matrix by controlling capital.

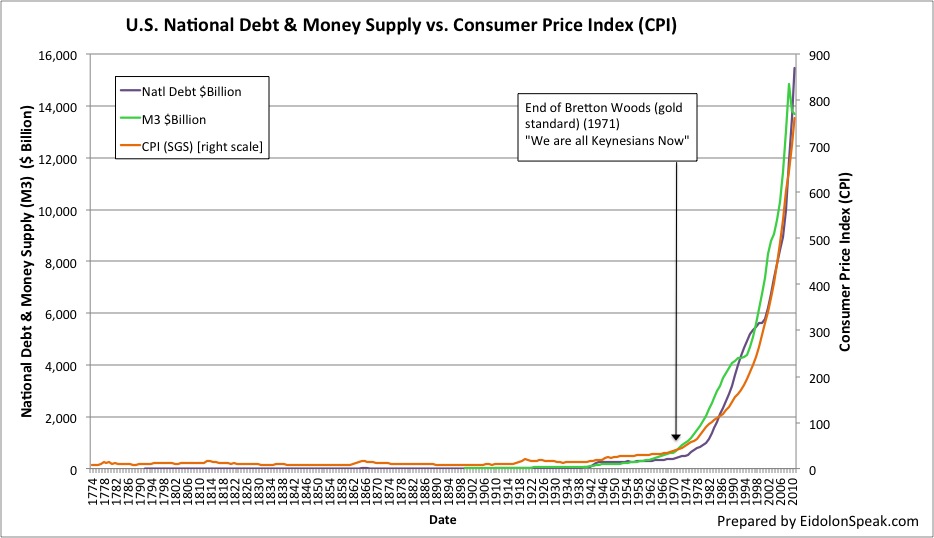

Unfortunately, however, the elites will not rest until they build a matrix to control the masses wealth. Hence, at the turn of the 20th century, the state and its elite cronies, broke through the gold-standard barrier and created the Financial Matrix. Through using fiat money (money not backed by gold or silver), the elites flooded the marketplace with bogus exchange values causing rapid inflation and rampant injustice. The Financial Matrix was birthed through a web of fractional-reserve banking (FRB), increasing national debts, and increasing taxes. One can recognize the extent of the monetary injustice caused by the Financial Matrix when studying what inflation has done to the value of the US dollar. For instance, the value of one dollar in 1913 is now worth less than four cents today. Or, said differently, one needs 25 dollars today to buy what one dollar purchased in 1913.

Inflation, however, is just one of the many injustices associated with the Financial Matrix. When inflation is combined with the increased personal and national debts (which result in an increase in taxation), one can see why the masses across the civilized world struggle to make ends meet. Indeed, the government-sponsored fractional reserve banking (FRB) system allows banks to partner with the central bank to create the majority of society’s money out of thin air. That’s correct, the FRB system permits banks to loan money into existence while the borrower must pay this fiat loan back with money he must earn through production.

In essence, artificial dollars are created without any real production and then loaned to people who must pay back the loan with interest from real production. Absurdly, the FRB system allows banks to create fake units of exchange that must be paid back by the borrower with real units of exchange plus interest. This is why the FRB system is the root of the new matrix of control and why the Financial Matrix is the most effective form of elites control ever developed. Moreover, the crony-capitalistic FRB system sets the low-interest rates which create the boom/bust cycle plaguing modern society. And, to add insult to injury, once the FRB system fosters the predictable boom/bust cycle, the boom is credited to the ingenious money controllers while the bust is blamed on the free markets. Apparently, its a loaded game of heads and tails where heads means the elites win and tails means the masses lose!

Although economists the caliber of Ricardo, Mises, and Von Hayek have insisted the FRB system is fraudulent and unstable, it survives through the masses ignorance and the elites support. Perhaps British Monetary Reformer, Michael Rowbotham, described the fraudulent nature of the FRB system the best when he wrote:

The creation and supply of money is now left almost entirely to banks and other lending institutions. Most people imagine that if they borrow from a bank, they are borrowing other people’s money. In fact, when banks and building societies make any loan, they create new money. Money loaned by a bank is not a loan of pre-existent money; money loaned by a bank is additional money created. The stream of money generated by people, businesses and governments constantly borrowing from banks and other lending institutions is relied upon to supply the economy as a whole. Thus the supply of money depends upon people going into debt, and the level of debt within an economy is no more than a measure of the amount of money that has been created…

In effect, today’s Financial Matrix relies upon millions of people voluntarily selling themselves into financial slavery. For when one combines artificially-low centrally-controlled interest rates to the FRB system, one has an irresistible combination that leads consumers and entrepreneurs to borrow money into existence. This money-creation, however, leads to the inflation. The inflation causes the boom/bust cycle when prices skyrocket. At this point, the consumers and entrepreneurs default on the loans they can no longer service and the bust wipes out the inflated values created during the boom. Not surprisingly, the boom/bust cycle occurred twice during the Greenspan-controlled central banking era. In both cases, the artificially-controlled low interest rates fueled the consumer’s appetite for speculation and “easy” profits. The internet bubble increased the Nasdaq nearly by a factor of five during the boom between 19995 and 2000, but it then preceded to collapse by over 60% between 2000-2001.

Regrettably, controllers seem to be perpetual optimist go from failure to failure without learning anything. As a result, when the twin-towers came crashing down, Greenspan repeated the same policy which caused the previous boom/bust cycle. This time, however, money poured into the housing markets and prices shot upwards of 50% in just a few short years. Not shockingly, the mortgage companies sought to maximize profits by helping everyone qualify for a home mortgage, even those who didn’t have steady jobs. The increase in mortgages exploded the money supply which further fueled higher priced houses and mortgages. The housing bubble was blowing up. Predictably, however, when the non-qualified borrowers could not make their mortgage payments, the housing bubble collapsed, the money supply collapsed, and the financial house of cards nearly followed them, but for government bail outs.

Above all, however, is the loss of house equities that have occurred since 1950. Disgracefully, the Financial Matrix has gutted the home-equity percentages (amount of value owned after subtracting all mortgages), decreasing home-equity percentages (percentage of ownership free from house loans) from over 80% to just over 30% today. This indicates that the Financial Matrix has gutted nearly 50% of the USA’s $25 trillion housing market in the last 60 years! That’s correct, nearly $12.5 trillion dollars (almost as much as the total USA national debt) lost by US citizens without so much as a whimper.

Americans sense something isn’t right, but few have a clue what it is, let alone how to fix it. Indeed, both the Occupy Wall Street and Tea Party movements formed as protests against injustice and exploitation. Protests without plans, however, usually leads to rebellion and peasant rebellions have a poor historical track records in generating positive change. Instead, the masses must learn to exit the Financial Matrix through a disciplined plan of financial defense and offense. This is why we formed LIFE Leadership and why we created the Financial Fitness Program – to teach people how to exit the Financial Matrix without violence. Remember, one is not coerced into the Financial Matrix, but rather enticed.

To me, the Financial Matrix is eerily similar to Neo’s discovery of the matrix in the movie called The Matrix. In several scenes, Morpheus reveals to Neo that the world is not as it seems. That a matrix controls the masses whether they are working, playing, or sleeping. The matrix is, “the world that has been pulled over your eyes, to blind you from the truth.” Neo, needless to say, asked what truth Morpheus was referring to and learns, “That you are a slave, Neo. Like everyone else, you were born into bondage, born into a prison that you cannot smell or taste or touch. A prison…for your mind….Unfortunately, no one can be… told what the Matrix is… you have to see it for yourself.” Morpheus places two pills before Neo and explains that if Neo takes the blue pill he will live an illusion and never escape the matrix, but if he takes the red pill, he will learn the truth about the matrix and learn how to set himself free.

If you, like Neo, have been searching for answers, the good news is: the search is over. The blue and red pills have been placed before you. Do you take the red pill, read the rest of the book, and learn how deep the rabbit hole goes or do you take the blue pill, set down the book, and believe the illusion of whatever you want to believe. Your destiny hangs in the balance. Choose wisely.

Sincerely,