Former Guinness World Record Holder for largest book signing ever, Orrin Woodward is a NY Times bestselling author of And Justice For All along with RESOLVED & coauthor of LeaderShift and Launching a Leadership Revolution. His books have sold over one million copies in the financial, leadership and liberty fields. RESOLVED: 13 Resolutions For LIFE made the Top 100 All-Time Best Leadership Books and the 13 Resolutions are the framework for the top selling Mental Fitness Challenge personal development program.

Orrin made the Top 20 Inc. Magazine Leadership list & has co-founded two multi-million dollar leadership companies. Currently, he serves as the Chairman of the Board of the LIFE. He has a B.S. degree from GMI-EMI (now Kettering University) in manufacturing systems engineering. He holds four U.S. patents, and won an exclusive National Technical Benchmarking Award.

This blog is an Alltop selection and ranked in HR's Top 100 Blogs for Management & Leadership.

The civilized world is the midst of a debt deluge; nonetheless, pessimism is not the answer. After all, although no one can control what governments or businesses do, everyone can stop being seduced into debt slavery. This alone would return 33% of the average person’s income back into his control and why defense is such an important part of financial literacy. Defense, simply stated, is spending less than one makes compounded over time. The difference between what one makes and what one spends is then applied to the current debt until all debts are eliminated. Amazing how simple it all sounds and also amazing how difficult it is to stop being seduced into slavery by the latest shiny object.

Interestingly, however, most financial literacy programs cover little, if anything, of the playing field and focus mainly on the defensive steps. While defense is good, no one can win a sports championship without offense also. Strangely, however, most programs are silent on the crucial aspect of the financial game. Hence, the typical financial education directs a person’s focus to his current reality. Naturally, this keeps his head down in the details and dirt of his current financial mess. The problem with financial mindset alone is it gets a person thinking so logically about scrimping today that he forgets to dream about a better tomorrow. In contrast, a proper financial plan should lead a person to look down into the details to develop today’s belt-tightening plan to be set into motion. Then, however, one must look up so he can get up. After all, the goal is not for a person to surrender all his dreams in order to live debt free. Rather the goal is for him to live below his means so he can begin investing, as Warren Buffett said, in his number one resource, namely, his personal development.

Indeed, developing personal and professional skills is essential for offense. Why this is not emphasized in a person’s financial plan is beyond me. Especially when one considers there are only two methods to increase the amount remaining between what one makes and one spends: either make more or spend less. As a result, both the make more (offense) and spend less (defense) are vital. To make more money, however, a person must dream for a better future and then invest in more skills. Did the reader catch the crucial distinction? The financial plan defense teaches to spend less while the offense teaches to invest more to develop marketable skills. Interestingly, the skills most highly prized are not the hard technical skills, but rather the soft people skills. For many gain the technical skills but lack the people skills to convey their ideas and work as part of a healthy team. Above all else, improved people skills is the fastest way to increase one’s income. For instance, Dale Carnegie once wrote, “…15 percent of one’s financial success is due to one’s technical knowledge and about 85 percent is due to skill in human engineering—to personality and the ability to lead people.”

Perhaps a person may believe that Carnegie’s quote, written back in 1936, is no longer valid in today’s highly technical age. However, if anything, people skills are more valued today than ever. For instance, even the technology giant, Google, realized that technical skills alone did not make for a good manager. According to Google Vice President Laszlo Bock, “In the Google context, we’d always believed that to be a manager, particularly on the engineering side, you needed to be as deep or deeper a technical expert than the people who work for you. It turns out that that’s absolutely the least important thing. It’s important, but pales in comparison. Much more important is just making that connection and being accessible.” This is the where the Financial Fitness Program shines above all others. For not only does it teach all the principles of defense, but also provides the best offense skills available through LIFE Leadership’s personal development library of products. The founders of LIFE have heard thousands of testimonies from people who have raised their incomes through increased commissions, job promotions, or improved effectiveness.

Be that as it may, this is still just the tip of the offense iceberg. The real secret of offense is to develop a burning desire. In contrast to getting buried in defensive details for the next 20 years, the Financial Fitness Program teaches a person how to dream and achieve. Perhaps there has never been a time in history where Napoleon Hill’s advice (he studied over 300 multi-millionaires before writing his classic Think and Grow Rich) is more needed than today: “There is one quality which one must possess to win, and that is definiteness of purpose, the knowledge of what one wants, and a burning desire to possess it.” Indeed, a burning desire turns fantasies into dreams and dreams into goals that are achievable. Unfortunately, most people live their lives as wandering generalities rather than one with specific intention. After all, success can be boiled down to three thoughts: 1) What do you want? 2) What’s it cost? 3) Pay it. The burning desire, needless to say, is what helps a person answer these three critical questions to help them live a life of purpose in an age of purposelessness. A burning desire turns a someday fantasy into a dream with a deadline through the power of goal setting set today. Success, like they said of Rome, isn’t built in a day, but it is built day by day.

Many people, when confronted with the reality of their financial positions respond like the ostrich hunted by a tiger and merely bury their heads in the sand. Others, in contrast, realize they must make some changes, but unfortunately, they get so mired in the defensive details that they lose the forest from studying the particular tree. Of course, both of these scenarios miss out on the true strength of the Financial Fitness Program (FFP). While many financial programs offer defensive strategies to get out of debt, only the FFP describes the playing field rules (Financial Matrix) and teaches how to win the financial game by combining defense and offense. After all, who wants to live on a financial diet the rest of their lives while sacrificing all their goals and dreams merely to be debt free? Is it possible to live debt free and still live the life of one’s dreams? This is EXACTLY why the FFP was created.

Financial Fitness Pack

First, the reader must understand the financial system is rigged against him. It’s not just a matter of the consumer lacking fiscal responsibility, although this certainly plays a part. In addition, however, the system itself is designed to profit the bankers at consumer expense. For example, whereas banks are allowed to create mortgage loans out of thin air (through the wonders of the fractional-reserve-banking system), people are expected to pay back this mortgage “money” by surrendering a portion of their productive labors over the course of the next thirty years or so. Of course, mortgage loans are just one of the avenues the banking system uses to secure its tentacles around a person’s pocketbook. Once student loans, car loans, car leases, credit cards, and consumer loans are added to the list, the amount of money going to service debt amounts to over 33% of a person’s take home income! Needless to say, paying 33% to the banking system for money created out of thin air seems like an unfair playing field.

Personal debt, however, is just one of the banking systems three-pronged approach to bilking society, for businesses and governments are also highly in debt to their eyeballs. In fact, the St. Louis Federal Reserve announced the total US debt (the combination of government, business, mortgage, and consumer debt) had increased from $2.2 trillion in 1972 (the year President Nixon took the dollar off the international gold standard) to nearly $59.4 trillion in the first quarter of 2014. That’s an unbelievable 27 times increase! Interestingly, the debt is split almost evenly among all three sectors with personal, business, and government debts totaling approximately$20 trillion each. Businesses cover their debt by raising prices while governments cover theirs by raising taxes; unfortunately, the consumer ends up footing the bill for both of these debts. No wonder citizens across the civilized world are struggling, for the compounding three-pronged parasitic debt attack does not rest.

Disastrously, even at just 5% interest, America’s interest on its debt today amounts to over $3 trillion. That’s 3,000,000,000,000 dollars! This interest money is siphoned off the top of the productive capacity of every American by the banking system that created it out of thin air. In other words, before anyone is allowed to enjoy the fruits of his labor, he is forced to service all debts (personal, business, and government). Like we said earlier, the game is rigged and participation in it only ensures financial failure in the long run. The authors termed this fixed game the Financial Matrix – a system of control designed to enslave people and profit the banking system. Unfortunately, the people’s lack of financial literacy allows the banking system to seduce the people into debt enslavement. The Financial Matrix, as a result, unlike earlier matrices of control based upon coercion like slavery or serfdom, is a matrix of control where people freely choose their own enslavement.

Perhaps 2016 is the year the reader decides to make changes for his financial future. LIFE Leadership‘s top selling product, the Financial Fitness Program, has already tracked nearly $6.5 million in debt reduction for its customers! The program and it will help the reader learn the defense, offense, and the playing field (Financial Matrix) for financial success.

You either hate losing enough to change or you hate change enough to lose. – Orrin Woodward

Why do some people seem to win at whatever they do while most settle for the middle of pack mediocrity? I believe the difference boils down to a person’s hierarchy of needs, namely, comfort or winning. On one hand, if comfort is the most important, then the person will resist all change regardless of whether it’s better because it’s uncomfortable. On the other hand, if winning is more important, then a person will get uncomfortable enough to improve to produce the results he desires. In a nutshell, winners are different because they refuse to settle for good when great is possible.

Change or Comfort?

I recently gave a keynote presentation where I played a classic 1988 Wendy’s advertisement that captured the key difference between those who win and those who simply work. It took less than 30 seconds for some advertising executive to pinpoint why most people don’t change. For many people are comfortable in past victories rather than uncomfortable in present mediocrity. Can my readers identify areas where they are settling for comfortable mediocrity rather than changing into uncomfortable champions? True, winning may not be as easy as some winners make it look, but I can promise you its not as tough as some losers make it sound either. 🙂

Simply put, the toughest part of winning is (dare I say it) getting comfortable being uncomfortable. Every day winners are pushed to get better because your competition never rest. Show me someone who is comfortable with an average scoreboard and I will show you someone who is one a downward slide. In contrast, show me someone who is already winning at the highest levels, but is still uncomfortable, and I will show you someone who is on their way to revolutionizing a their chosen field. LIFE Leadership CEO Chris Brady and I have vowed to stay hungry, honorable, and honorable on our way to helping millions of people escape the Financial Matrix!

I am embedding the Wendy’s ad for your viewing pleasure. What is your takeaway from the video?

Several weeks ago, I was asked to be a guest on the financial education site Rethinking the Dollar to discuss my new book The Financial Matrix. The interviewer asked some great questions (and despite some internet issues) the content should help citizens from across the world in their quest to be debt-free.

Many people believe that money and financial literacy is not really that important. However, I’m not sure how to respond to this since nearly everyone who tells me this also later admits to me that they are in debt personally. This seems absurd to me. If money truly isn’t that important, then why sell yourself into debt slavery to obtain such a trivial item? Ouch! I know that’s quite a truth bomb, but think about it – if money really wasn’t that important then there would be a lot less debt! People speak foolishly when they buy their own lies and then start selling them to others. Does anyone else see the hypocrisy of spending more time working for money than investing time with family and friends and yet still claiming money isn’t important? Especially when we remember that the best way to read a person’s mind is through their actions and the actions and words simply aren’t aligning in most people’s lives.

The truth of the matter is that family and friends are much more important than money, but because the masses lack financial literacy, the elites control the masses through the masses ignorance. For instance, I don’t believe one in a thousand people can accurately explain what money is; nonetheless, the average person will spend over 40 hours per week for nearly 50 weeks per year for over 40 years in a quest to accumulate the object they cannot even define. Believe me, I am not knocking the reader when I say this because it is exactly the same position Laurie and I were in when we awoke from our fog. We asked ourselves, why are we spending so much of our life seeking something we do not even understand (money), let alone love. We were not seeking money for its own sake, but rather for the choices, charity, and security it could provide for our family.

At any rate, in a capitalistic society, money rates close to oxygen in the hierarchy of needs. Interestingly, you rarely hear someone say that oxygen isn’t important to them. 🙂 In fact, classic historian Augustus Boeckh, described money’s importance in ancient Athens when he noted, “The intellectual faculties however are not of themselves sufficient to produce external action; they require the aid of physical force, the direction and combination of which are wholly at the disposal of money, that mighty spring by which the total force of human energies is set in motion.” Money, in short, is power because it can requisition whatever resources necessary to accomplish the owners objectives.

As a result, when society surrenders its money to the Financial Elites, it soon loses the media and military to the elite manipulation when they use the easy money to buy them as well. Suddenly, the once free nation has now become a subjugated State where puppet politicians serve the Financial Elites rather than the people. Yes, the Financial Matrix rabbit hole continues to go deeper every time I study it. Even so, I will continue to study and ask the tough questions so long as I have the freedom to do so. Simply put, in a capitalist society, he who controls the money controls the society. Hence, the only way to regain our freedoms is to restore the free enterprise system to money where the price of the commodity (interest rate) is determined by the supply and demand for money in the marketplace.

What can the readers do to help restore freedom? For starters, they can educate themselves by applying the principles taught in the Financial Fitness Program. LIFE Leadership is on a mission to educate the masses around the world on the importance of financial literacy. You will either master money or money will master you. When money becomes your master, the person typically responds by becoming the King or Queen of Denial, claiming the money idol has no control over his/her life while it increasingly enslaves them in a web of debt and despair.

Thankfully, for those who are willing to look honestly at their financial situation, there is a path to freedom. Indeed, the birth of new knowledge begins with an admission of old ignorance. Laurie and I were ignorant in financial literacy and thus had entrapped ourselves in the Financial Matrix. Indeed, it was only once we realized our error that we sought better information to free ourselves from financial slavery.

Maybe 2016 is the year you make the change from debt slavery to debt freedom. If the reader is ready, I suggest you begin by diving into the Financial Fitness Program and start the journey of setting your family free! I hope you enjoy the video below.

“The great question which in all ages has disturbed mankind, and brought on them the greatest part of those mischiefs which have ruined cities, depopulated countries, and disordered the peace of the world, has been, not whether there be power in the world, nor whence it came, but who should have it.”– John Locke – First Treatise of Government

Power, as John Locke inferred, is an omnipresent force in the world. The strong, from the creation of mankind, have ruled over the weak, subjecting them to various degrees of oppression. Although many believe the worst is behind us with the end of slavery and serfdom, this may not actually be the case. For the modern Big Bank/Big State/Big Business marriage, known as Crony Capitalism, has increased the elites’ control over the weak through the power of leveraged debt. This subtle form of coercion (through the fear of debt collectors harassment, mortgage defaults, and bankruptcy proceedings) forces many people into the purposeless quagmire of long hours, loads of stress, and yet little real ownership. In effect, today’s indebted people do not work to own anything but merely work to service debt. This, however, is historically little different than the slave or serf was also coerced into working without owning. No wonder Solomon once wrote, “There is nothing new under the sun.”

Whereas Slavery was a Physical Matrix of control and Serfdom was a Feudal Matrix of control, what should we call the financial subjugation of society? I termed it the Financial Matrix and I believe it’s the elites most powerful matrix of control yet. Why? Because few people even know it exist let alone know how to resist it. While a slave knew he was enslaved physically and a serf knew he was trapped on the lord’s land, few comprehend that debt traps a person to the financial lords. In other words, a person in the Financial Matrix is enslaved and yet believes he is free; in consequence, escaping the web of debt is very difficult because he is not even aware he has been captured. The elites, on the other hand, understood quickly the benefits of the masses feeling free while actually being entrapped by their lack of financial literacy. The Financial Matrix, in other words, ensured the masses worked harder and longer than slaves or serfs were while reaping little longterm rewards. Simply looking at the statistics of the average person’s wealth at 65 is enough to demoralize anyone. How can the masses work that long and have so little to show for it? Simply put, a lack of financial literacy entraps them into the Financial Matrix the benefits the elites and breaks the masses.

The economist Henry Macleod highlighted the power and influence debt money has had upon society when he noted, “If we were asked – Who made the discovery which has most deeply affected the fortunes of the human race? We think, after full consideration, we might safely answer – The man who first discovered that a Debt is a Saleable Commodity.” The importance of Macleod’s statement cannot be overemphasized because until the reader understands its underlying message, he will think I am exaggerating the effects of debt upon people’s freedoms. Nonetheless, no less an authority than Ludwig Von Mises (one of the early members of the Austrian School of free market economics), pointed out the key differences between commodity money and debt money. Mises defined money as simply society’s most in demand commodity (typically silver or gold).

The free market has never chosen paper bank notes as its money of choice freely. Hence, when the banking system discovered they could make debt a saleable commodity, it needed to partner with the State and use its “monopoly of force” to coerce society into using debt money through passing legal tender laws. Not surprisingly, the States gladly accepted the cheap debt money created out of nothing by the Big Banks and then forced society to do the same. This is a win for the Big Banks (massive interest profits) and a win for the States (massive increases in power from access to funds) and a massive loss to society in increasing debt and inflation while decreasing the people’s freedoms. As a result, the Financial elites now control the State and the State controls society (the same old story of the strong oppressing the weak) through the Financial Matrix’s system of control.

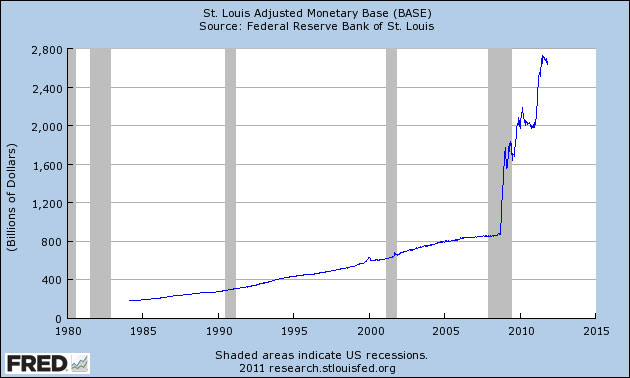

Federal Reserve Massive Increase in Fiat Money

Author Felix Martin noted in his interesting book Money, “For credit to become money, sellers must also trust that third parties will be willing to accept the debtor’s IOU in payment as well. They must believe that it is, and will remain indefinitely, transferable – that the market for this money is liquid. Depending upon how powerful are the reasons to believe these two things, it will be easier or harder for an issuer’s IOUs to circulate as money. It is because of this third critical element of transferability that money issued by governments, or by the banks which governments endorse and backstop, is thought to be special. Indeed, there is an influential school of thought – known as chartilism – which argues that governments and their agents are the only viable issuers of money.”

Martin, although brilliant in his historical analysis, is an apologist for the Financial Matrix and supports Statism in monetary matters (State intervention into society’s money). Thus, it’s not shocking he supports the State’s role in legalizing and supporting the creation of debt money. In reality, the State must get involved if debt money is to survive in society, for no one would accept the bank notes without the State’s unnatural coercion. Again, this is nothing less than State coercion over society to for the benefit of the strong (Financial and Political Elites) over the weak (the masses). Interestingly, however, when the State collapses the paper banknotes return to their true value – nothing. State force, in other words, is the only thing that props up the value of the fiat paper notes. A true commodity money, as Mises points out, does not need State intervention to prop up its value because it marginal utility is determined by the market, not a dictating State. All the State needs to do in a free market system is define the amount of gold and silver in its monetary unit. Then, the State should ensure the weights and measurements remain unchanged. Of course, the marginal value of the monetary unit will change as the production and consumer demand for money changes, but the standard itself should never change.

Federal Reserve Bank Notes Increase

The money supply will change slightly as more gold is discovered, but not anything close to the amount it changes in the Financial Matrix. For instance, the total value of the gold and silver mined during the entire time the Spanish controlled its South American colonies was approximately $250 billion. In comparison, the Federal Reserve increased the money supply by $250 billion in digitized debt in just one day during the 2008 Great Financial Crisis. What took the Spanish State over 250 years to accumulate, in other words, the Federal Reserve accomplished in mere milliseconds! Disastrously, the State’s “monopoly of force” is no longer used to ensure justice for its citizens, but rather to ensure Financial Matrix injustice. How do you win an argument against a person who has a gun pointed at your face? No matter how logical or reasonable your position is, the person with the gun always gets his way. In a similar fashion the State always wins an argument regardless of how illogical its position is. 🙂 Does the reader now understand why its absurd to surrender control of the money supply to the Big Banks/Big States Financial Matrix?

Banker apologist, Felix Martin, concluded, “If money was such a powerful invention – such a revolutionary force for the transformation of society and the economy – the next question is obvious. It is one posed with brilliant clarity by the father of English political philosophy. It is to the perennial battle over who controls the money that we therefore turn next.” Martin, in reality, has posed the wrong question. And, when someone asks the wrong question, he rarely receives the right answer. The real question is – why does anyone need to control the money supply? Why not let the market determine the commodity, quantity, and price of money just as it should all other commodities? Isn’t this the definition of a free market and freedom for the people? A free market is where no one controls the supply or price of any commodity within society; instead, the marketplace (consumers) determine demand, supply and price based upon the sum of the individual valuations.

We are fast approaching the end of the road and we only have one fork remaining. Down the current path is the Hayekian road to serfdom while the last for is the path returning to freedom. Unfortunately, most people spend their whole life working for money, all the while, remaining ignorant as to what money is and how personal debt controls them.LIFE Leadership has vowed to right this wrong by by sharing the Financial Fitness Program principles of financial literacy with the masses. I can think of no better way to fulfill my God-given purpose than to take the principles Laurie and I learned to break free from the Financial Matrix and teach them to others. It’s time for LIFE Leadership to set millions of financial captives free!

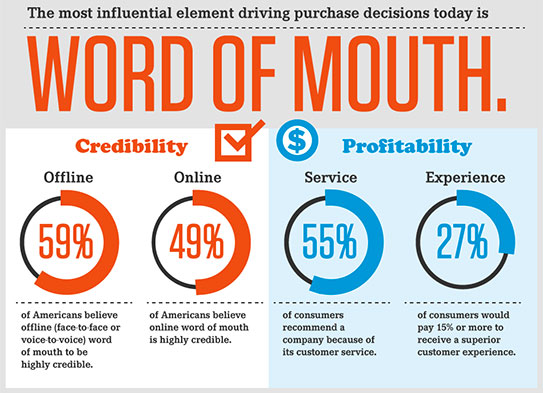

Word of Mouth advertising is the most effective form of advertising and thus why LIFE Leadership leverages the concept through its Compensated Community to spread its message. The Financial Matrix looms larger everyday for those without financial literacy. Thankfully, however, there is a community of people who are doing something about it. Below are some thoughts I am working on about Word of Mouth marketing.

LIFE Leadership leverages word-of-mouth marketing to compound its growth. Instead of paying millions of dollars per year to advertise in print, radio, or TV, LIFE Leadership instead rewards people who recommend our products. This is a major competitive advantage! For example, authors Huba and McConnell proclaimed, “Word-of-mouth is THE valuable currency in today’s advertising-saturated world.” Meanwhile, Nielsen Global Trust in Advertising noted that 92% of respondents surveyed trusted recommendations received from friends about products or services. Last but not least, a recent McKinsey study identified word-of-mouth as the most effective form of marketing and advertising in the world. According to the McKinsey study, word-of-mouth marketing generates twice as much sales as paid advertising, and over 50% of all purchases are influenced by word-of-mouth. Indeed, the buzz generated by word-of-mouth marketing is vital to the growth of a company.

Because word-of-mouth marketing is so effective, LIFE Leadership built all of its marketing and advertising budget around it. We reward loyal customers and members who are effective in recommending our products to others. All word-of-mouth marketing can be boiled down to a three-step process:

1. Discovery: Somebody encounters a new idea.

2. Wow: This person is convinced that the idea is worth sharing.

3. The Share: The person shares the new information with others.

Once this process loop is started, the share stage for one person corresponds with the discovery stage of another one, and the word-of-mouth chain reaction has started. Seth Godin, author of Unleashing the Ideavirus, emphasized the importance of making it easy to share the product or company’s message: “How easy is it for an end user to spread this particular ideavirus? Can I click one button or mention some magic phrase, or do I have to go through hoops and risk embarrassment to tell someone about it?”

A big secret to life is when you discover that learning is just as enjoyable as entertainment is, but with long term benefits. – Orrin Woodward

In the process of researching for my second book in the And Justice For All series, I stumbled across one of the most profound descriptions of the importance of education in a person’s life by Professor Ernest Barker. As I read the words below, I realized how important LIFE Leadership is in improving society. For LIFE helps people focus on achievement through a process of eliminating debt and building a community through serving others by pursuing wisdom and leadership. In effect, the size and speed of the results achieved is a measurement of the wisdom applied to their life and business. The Bible teaches clearly that all true wisdom begins with fear of the Lord and that Christians should seek righteousness and all others things will be added.

Unfortunately, however, few people apply these Biblical lessons consistently. Despite the numerous historical examples of people who applied Biblical wisdom to life and were blessed beyond measure, many still chase money rather than wisdom. In a capitalistic system, money flows to those who apply wisdom to business, but the reverse of this is not true – wisdom flows to those with money. For instance, Laurie and I have many monetary blessings, but none of these satisfy like sharing wisdom with others to stimulate breakthroughs in mentoring sessions or the “aha” moments of self-discovery when the veil of ignorance is removed and one sees clearly the principles to apply to move ahead. Indeed, once a person becomes a seeker of knowledge, he will never be bored again because there is always more wisdom to learn and apply. I love my life and wouldn’t trade places with anyone else because I have been blessed with the leisure to learn and grow. Even more importantly, I am blessed to share what I have learned with other hungry students seeking wisdom in life.

The Financial Matrix is a system of control designed to enslave people in their own ignorance. Hence, if one wished to escape the matrix, one must escape not only physically, but also mentally. To do this, a person must build a business asset to buy back his time because only then will he have the leisure to invest in a self-directed education to develop wisdom. LIFE Leadership is the vehicle to accomplish this where people can live their dreams by losing their debt? However, living your dreams requires a plan and a willingness to work hard. What is the reader’s plan to develop wisdom and seek righteousness? These two steps are foundational to having everything else added unto him to live his/her dreams. I pray you achieve all the success you earn.

Our modern economic society, we have seen, requires leisure and education as its complements and its correctives. They are two things which should go together. Leisure is a time to be devoted — not wholly, for the body has its claims to relaxation, and the mind too needs its gentle indulgences ; not wholly, but at any rate largely — to the purposes of education and the gaining of that knowledge, not to be acquired in the course of work, ‘which brings wisdom rather than affluence.’ Education, on the other hand, should be a training — not again wholly, but at any rate largely — in the right way of using leisure, which without education may be misspent and frittered away. This vital connexion between leisure and education is a fundamental thing. Unless we grasp it, we are in danger of abusing leisure and misusing education. And in order that we may grasp it, it is necessary that we should have a right conception of the meaning of leisure;

One of the old Greek philosophers made a distinction which may help us here. He thought that we ought not merely to distinguish between work and leisure, but also to distinguish between leisure and recreation. Work, he thought, was something done not for its own sake, but as a means to something else — affluence, let us say, or at any rate subsistence ; recreation was rest from work, which took the form of play, and issued in the recovery of the poise of body and mind, disturbed and unbalanced by work ; but leisure was a noble thing, and indeed the noblest thing in life ; it was employment in some activity (we may almost say some form of work) which was desirable for its own sake such as the hearing of noble music and poetry, intercourse with friends chosen for their worth, or the exercise of the speculative faculty.

In this fine sense of the word, we may say that we live for leisure ; that it is the end of our being, which transcends work and far transcends recreation ; that it is the growing time of the human spirit, which in its leisure from necessary toils, and the necessary recreations they entail as their counterpoise, can expand in communion with its own thoughts and with the thoughts of others and with the Grace of God. The sad thing about modern English society is that there is so little leisure in this higher sense. It is not only that we work so hard : it is also that we play so hard. Perhaps the monotony and uniformity of work sends us in reaction to the hazards of games, or the excitement of watching them, or the still greater excitement of betting upon them : perhaps the urban aggregations in which men now live make them unhappy unless they are crowding together to some common game or spectacle.

Whatever the reason, poor leisure is far too often out in the cold, while recreation is romping about all the rooms in the house. One need be no kill- joy or Puritan to think or talk in this strain. Life is something more than a series of alternate layers of lean work and fat hearty play. It is meant for the growth and development of the human spirit. And that growth needs its growing time, which is leisure. If leisure be largely for education, education is also largely for leisure. We too often think and speak of education as something intended to fit us for life’s work. Ideally, it should rather be intended to fit us for life’s leisure. I do not mean that education should be humane rather than vocational.

Education may be humane, and yet directed to work and the better doing of work. I mean something more — that education should mean the filling of our mind with interests and possibilities of high delight, which we can develop for ourselves in all our leisure hours ; that it should be an initiation in the tastes and pursuits which will crown our leisure with fulfilment ; in a word, that it should be a training and a preparation for the right use of the time of the spirit’s freedom. Perhaps education has not hitherto been sufficiently adjusted to this end. Perhaps, if it had been, it would have been directed more to the awakening of a taste for art and music, in order that they might become the permanent possession and the abiding joy of later years.

Be that as it may, it is surely true that education is a necessity if men are to gain the faculty of using leisure easily, happily, and fruitfully. The use of leisure is a difficult thing. The majority of us, when freedom is given into our hands, fly to the excitement of some form of recreation. We must be ‘doing’ something — preferably something physical : if we are not, we are lost and without resource. We know the routine of work : we know the rules and the routine of different forms of play ; but we do not know how to move freely, originally, and by our own choice in the world that lies above work and play — the world of leisure. This is why holidays sometimes pall, and leave us at a loss : it is why men who have retired from work sometimes fall into melancholy, and find their reason for living gone.

Leisure without faculty for its use may even be a mother of mischief; men may dissipate themselves in frivolities, and worse than frivolities, because they do not know how to concentrate themselves upon better things. A society which guarantees leisure is guaranteeing something which may be useless, and even dangerous, unless it adds, or at any rate encourages its members to add, the one thing which will enable the gift to be used — a continuous process of education.

The world offers to the mind of man many noble joys. There is a joy in knowing the flowers of the field, and calling them by their names. There is a joy in knowing tlie heavenly bodies which move above us, and in understanding the rhythm and the rules of their motions. There is a joy in knowing the past of our kind, and in unrolling the long record of human history which explains what we are to-day. There is a joy in entering into the vision of the poet and painter, who have seen the ideal beauty which is hidden from ordinary eyes. There is a joy in wrestling with the thought of great philosophers, who have pondered about the why and wherefore of this mortal world and our mortal existence in it. These are the joys of leisure ; and leisure is the growing time of the spirit because it is the time of these joys. But it needs an effort to catch these joys ; and you cannot catch them without hooks of apprehension.

You must know a little in order to want to know more. Blank ignorance is blank incuriousness, but a little knowledge may be the opportunity and the incentive for more knowledge. The facts presented to mere ignorance are facts which there are no hooks to catch ; but when a mind has had some little training, it develops tentacles of apprehension ; it is anxious to seize new stuff, to arrange it and co-ordinate it with the old stuff which is already there, and so to make a little systematic world of its own for its own high delectation. The mind which is furnished with these tentacles and hooks of apprehension is a mind which will never be embarrassed or dumbfounded by leisure.

It will begin to play at once, in the nobler sense of the word play: the hooks will grip more and more of things seen and unseen into its consciousness ; and in the growing time there will be growth. When we say, therefore, that education is a preparation for the enjoyment of leisure, we mean that it is an equipment of the mind with these hooks and tentacles, these curiosities and appetites. And from this point of view we may see that there is a large sphere for the education of the adult, and that education is in no sense only the concern of childhood. The child learns at school ; but the child learns at a time when real experience of life has not yet begun. He learns, and is often curious to learn ; but what he learns cannot be co-ordinated with, or grappled into, a first-hand experience, because such experience has not yet begun to be gathered.

When he goes out into the world, and begins to gather experience, that experience may seem to him the one essential thing, and the school time lessons may fade away into the outgrown occupations of a vanished childhood. It is at this age — the age of adolescence, young manhood and young womanhood — that everything turns on the rescue of young minds from being immersed in mere experience. It is now that they need to recover curiosities, and to be furnished with hooks and tentacles of apprehension, by which they can capture a knowledge which can now be co-ordinated with experience. History, for example, is one thing to a child — a record of exciting events which satisfies curiosity : it is another thing to an adult — a record of the moral experience of men and nations which can be compared with and interpreted by the moral experience which the adult has himself gone through.

But unless, in adolescent and adult years, the curiosity be reawakened and recovered, the adult mind may remain immersed in its own more immediate experience ; and the high contemplation which lifts it above such experience, and yet explains and interprets that experience, may never be attained. Adolescent and adult education are in this way of primary importance, if man is to rise to that height of his being in which he uses leisure for the purpose of contemplation of the world, in order to explain it, and his own experience of it, and to attain to the justification of faith in its purpose and operation.

The perpetual booms and bust we see in Capitalism are not caused by the free market. Rather, they are the direct result of interventions in the natural rate of interest by Big Banks and the State (yes, it’s the dreaded Financial Matrix). These centrally planned interventions into the free markets cause the booms and bust, but in an ironic twist, the free market is blamed when the predictable dismal outcome occurs. Hence more central planning is proposed to fix the allegedly broken free market. The illogicalness of this argument almost makes me lose my emotional intelligence. 🙂

For it reminds me of the story of a drunk suffering from a hangover who blames his pain, not on too much drinking, but rather believes his body’s natural systems are imbalanced. Thus, he surmises to drink even more because he must make up for his body’s deficient natural system. When the pain goes away temporarily, he proclaims his intervention successful because he is pain-free. Unfortunately, the party (boom) always ends and when tomorrow morning hits, the cycle will repeat itself with even more rationalizations about the inherently unstable bodily systems and the need for more drugs. Of course, this leads to even worse cycle of temporary joy and longterm pain until the drunk either wizens up or dies. I wish I were exaggerating here, but the drunk’s logic is the same as our modern day politicians and economists (owned mouthpieces of the Financial Matrix controllers) who increase interventions into the economy which cause increasingly disruptive boom/bust cycles.

Nonetheless, further government intervention within the free market is always the answer when the previous intervention fails. Regretfully, many seemingly intelligent people buy into this line of thinking because it is promoted across the mainstream media outlets by the hired hands of the elites. As for me, I could care less how many “authorities” state their opinions because no matter how many people with whatever titles say something foolish, it’s still foolish. Even a majority doesn’t change this because foolish plus foolish is foolish, not wisdom. As an aside, if anyone is seeking rational discussion on this subject, he or she need look no further than de Soto’s fantastic book on money, banking, and business cycles displayed on this blog post.

To wet your appetite, I will attach a short description of the Austrian Business Cycle theory that I found online. In my nearly 15 years of research into the Austrian School of economics, I have not found an economic philosophy that reasons clearer and states the facts better regardless of the political costs than this group does. LIFE Leadership is on a quest for truth and the Austrian School has much truth to share.

The article below was written by Ben Best and describes the Austrian Business Cycle Theory:

Austrian Business Cycle

Austrian analysis asserts that in a world of hard money and free banking, the inflationary forces of credit expansion due to fractional reserve banking would not exist. If banks were warehouses of commodity money — gold, for example — then currency would consist of bank notes representing claims on the gold held by a bank. Any bank that made loans in excess of its reserves (fractional reserve banking) would soon find itself insolvent when other banks demanded hard money in exchange for checks & banknotes issued by that bank. This effect on banks is entirely analogous to the effects on countries that occurred after World War I when most nations attempted to implement a fractional reserve gold standard for their currencies. Countries issuing large amounts of currency backed by small amounts of gold found themselves in trouble when other countries sought to exchange currency to obtain gold. (See History of Modern Monetary Standards.) Banks in a free banking system would face similar pressures against fractional gold backing for their banknotes.

According to Austrian Economists, fractional reserve banking only became possible through the outlawing of private money and the creation of central (ie, government-controlled) banks — which allowed governments to control money supply and bank credit expansion.

In a free market interest rates are determined by subjective time-preference and the supply & demand of loanable money. If there is a low rate of savings the quantity (supply) of loanable money will be low and competition for this money (demand) by potential borrowers will result in high interest rates. High interest rates will encourage more savings and thereby bring the price of loans (interest rates) downward. As with supply & demand for any good or service, a free market will find a “clearing price” for the supply & demand of loanable funds. This clearing price is the natural rate of interest.

The natural rate of interest plays an extremely important role in the capital structure of an economy. Entrepreneurs/capitalists base decisions on whether to begin long-term capital projects based on interest rates. If interest rates are low, then borrowing to build a new factory, invest in a telecommunications network or assemble the capital goods for a new business venture appears feasible. Supply & demand of loanable funds will respond gradually to adjustments in business activity. If business investment (competition for loanable funds) rises, so too will interest rates — reducing borrowing for investment.

Central bank control of money & short-term interest-rates in national economies is at the root of contemporary business cycles. (For background on the mechanics of short-term interest-rate manipulation by central banks, see Money-Creation by Banks and A “Managed Economy” Under the Federal Reserve System.) When central banks artificially lower short-term interest rates below natural market levels, this results in two major distortions in capital markets. First, those who would save money receive less than the natural rate of interest — and this disincentive to save actually reduces the amount of loanable funds in real (as distinct from nominal) terms. Second, those who would borrow money for large capital projects are paying less than the natural rate of interest — thus encouraging borrowing investors to believe that capital projects are more sustainable than they really are.

Artificial lowering of interest rates by central banks is thus accompanied by expansion of the money supply — resulting in an artificial stimulus to spending for both consumer goods and capital goods. This artificial stimulus results in an inflationary boom which is not sustainable. Central banks are ultimately forced to raise short-term interest rates to counteract the inflation, resulting in a bust. Supporters of central bank monetary manipulation justify the practice as a means of leveling-out the business cycle when, in fact, central banker monetary manipulation is the cause of the business cycle!

In the 19th century, when money was based on gold & silver rather than government fiat, economic growth was mildly deflationary — because increased productivity lowers production costs. Inflation follows from government expansion of money supply and is not the result of an “overheating” economy that is growing rapidly. A distinction should be made between non-inflationary economic growth due to enterprise & technology and inflationary unsustainable booms due to central bank interest-rate cuts. Lack of clarity about this distinction has misled many economists into believing that there is an upper limit to growth (about 3%) above which growth is inflationary and unsustainable. Artificially low interest rates increase consumption spending, reduce incentives to save and increase investment spending with new fiat money that creates the illusion of new wealth. After having expanded the money supply with credit-expansion, central bankers worry that economic growth is “overheating” the economy, and the bankers then increase interest rates to “fight inflation”.

I love providing a business where everyone has an equal opportunity. No one should be hindered from progressing towards their dreams because of race, religion, or sex so long as they also do not hinder others. Unfortunately, the proper quest for equal opportunity has now morphed into an unjust demand for equal results. This is not only impossible physically, but extremely dangerous metaphysically. For the only way to create equality of results is to coercively take private property from some to give to others. In other words, in the quest for equality of results, the quest for liberty and justice is thrown out the window.

As Chairman of the Board of LIFE Leadership, I know everyone who enters our business has equality of opportunity (they have the same compensation plan), but also know the results will vary based upon efforts, people skills, and leadership abilities. Thankfully, even if one starts out with little abilities in any of these categories, with persistency, he or she can still climb to the top. In effect, it’s not how bad a person is when they start that matters as much as how willing he/she is to change. If the dream is big enough, a person can change until the “facts” are in his/her favor. Indeed, I have seen this process occur many times in the LIFE Leadership community.

This, however, would all change if government were to mandate equality of results rather than equality of opportunity. For anytime equality of results is enforced, what ensues is a race to the bottom as each person seeks to do the minimum amount possible since no extra efforts are rewarded. This has been proven historically by the failure of every communist regime to even feed its people let alone prosper. Below, I attached a short article on the Greek myth Procrustes and a short section of Murray Rothbard’s brilliant article on inequality. Please share your thoughts below.

Procrustes is the legendary Greek robber dwelling somewhere in Attica. Procrustes had an iron bed on which he compelled his victims to lie. Here, if a victim was shorter than the bed, he stretched him by hammering or racking the body to fit. Alternatively, if the victim was longer than the bed, he cut off the legs to make the body fit the bed’s length. In either event the victim died. Ultimately Procrustes was slain by his own method by the young Attic hero Theseus as a young man slayed robbers and monsters whom he encountered while traveling from Trozen to Athens. The “bed of Procrustes,” or “Procrustean bed,” has become proverbial for arbitrarily—and perhaps ruthlessly—forcing someone or something to fit into an unnatural scheme or pattern.

The New Coercive Elite

Procrustes Equality

When we confront the egalitarian movement, we begin to find the first practical, if not logical, contradiction within the program itself: that its outstanding advocates are not in any sense in the ranks of the poor and oppressed, but are Harvard, Yale, and Oxford professors, as well as other leaders of the privileged social and power elite. What kind of “egalitarianism” is this? If this phenomenon is supposed to embody a massive assumption of liberal guilt, then it is curious that we see very few of this breast-beating elite actually divesting themselves of their worldly goods, prestige, and status, and go live humbly and anonymously among the poor and destitute. Quite the contrary, they seem not to stumble a step on their climb to wealth, fame, and power. Instead, they invariably bask in the congratulations of themselves and their like-minded colleagues of the high-minded morality in which they have all cloaked themselves.

Perhaps the answer to this puzzle lies in our old friend Procrustes. Since no two people are uniform or “equal” in any sense in nature, or in the outcomes of a voluntary society, to bring about and maintain such equality necessarily requires the permanent imposition of a power elite armed with devastating coercive power. For an egalitarian program clearly requires a powerful ruling elite to wield the formidable weapons of coercion and even terror required to operate the Procrustean rack: to try to force everyone into an egalitarian mold. Hence, at least for the ruling elite, there is no “equality” here — only vast inequalities of power, decisionmaking, and undoubtedly, income and wealth as well.

Thus, the English philosopher Antony Flew points out that “the Procrustean ideal has, as it is bound to have, the most powerful attraction for those already playing or hoping in the future to play prominent or rewarding parts in the machinery of enforcement.” Flew notes that this Procrustean ideal is “the uniting and justifying ideology of a rising class of policy advisors and public welfare professionals,” adding significantly that “these are all people both professionally involved in, and owing to their past and future advancement to, the business of enforcing it.”

That the necessary consequence of an egalitarian program is the decidedly inegalitarian creation of a ruthless power elite was recognized and embraced by the English Marxist-Lenist sociologist Frank Parkin. Parkin concluded that “Egalitarianism seems to require a political system in which the state is able to hold in check those social and occupational groups which, by virtue of their skills or education or personal attributes, might otherwise attempt to stake claims to a disproportionate share of society’s rewards. The most effective way of holding such groups in check is by denying the right to organize politically, or, in other ways, to undermine social equality. This presumably is the reasoning underlying the Marxist-Leninist case for a political order based upon the dictatorship of the proletariat.”

But how is it that Parkin and his egalitarian ilk never seem to realize that this explicit assault on “social equality” leads to tremendous inequalities of power, decisionmaking authority, and, inevitably, income and wealth? Indeed, why is this seemingly obvious question never so much as raised among them? Could there be hypocrisy or even deceit at work?

“The only man who sticks closer to you in adversity than a friend is a creditor.”

It’s impossible to consistently win in any endeavor without a plan. Unfortunately, most people in life do not have a financial plan; therefore, they struggle financially. The Financial Fitness Program is a step-by-step plan to help someone develop a plan for defense, offense, and understanding the playing field (The Financial Matrix) of financial success.

Why start at zero and have to spend years learning the principles of financial success when a person can invest $99 dollars and have access, not only to a winning financial plan (thousands have eliminated their credit card debt), but also the LIFE Leadership community to help one stay accountable to his/her goals and dreams? Life is tough inside the Financial Matrix. That is why a supportive community of people with the same objective – to escape the Financial Matrix – is so vital.

Here is a segment of a talk I gave in Wisconsin on the importance of having a plan, working the plan, and persisting in the plan until victory.

Interestingly, however, most financial literacy programs cover little, if anything, of the playing field and focus mainly on the defensive steps. While defense is good, no one can win a sports championship without offense also. Strangely, however, most programs are silent on the crucial aspect of the financial game. Hence, the typical financial education directs a person’s focus to his current reality. Naturally, this keeps his head down in the details and dirt of his current financial mess. The problem with financial mindset alone is it gets a person thinking so logically about scrimping today that he forgets to dream about a better tomorrow. In contrast, a proper financial plan should lead a person to look down into the details to develop today’s belt-tightening plan to be set into motion. Then, however, one must look up so he can get up. After all, the goal is not for a person to surrender all his dreams in order to live debt free. Rather the goal is for him to live below his means so he can begin investing, as Warren Buffett said, in his number one resource, namely, his personal development.

Interestingly, however, most financial literacy programs cover little, if anything, of the playing field and focus mainly on the defensive steps. While defense is good, no one can win a sports championship without offense also. Strangely, however, most programs are silent on the crucial aspect of the financial game. Hence, the typical financial education directs a person’s focus to his current reality. Naturally, this keeps his head down in the details and dirt of his current financial mess. The problem with financial mindset alone is it gets a person thinking so logically about scrimping today that he forgets to dream about a better tomorrow. In contrast, a proper financial plan should lead a person to look down into the details to develop today’s belt-tightening plan to be set into motion. Then, however, one must look up so he can get up. After all, the goal is not for a person to surrender all his dreams in order to live debt free. Rather the goal is for him to live below his means so he can begin investing, as Warren Buffett said, in his number one resource, namely, his personal development.